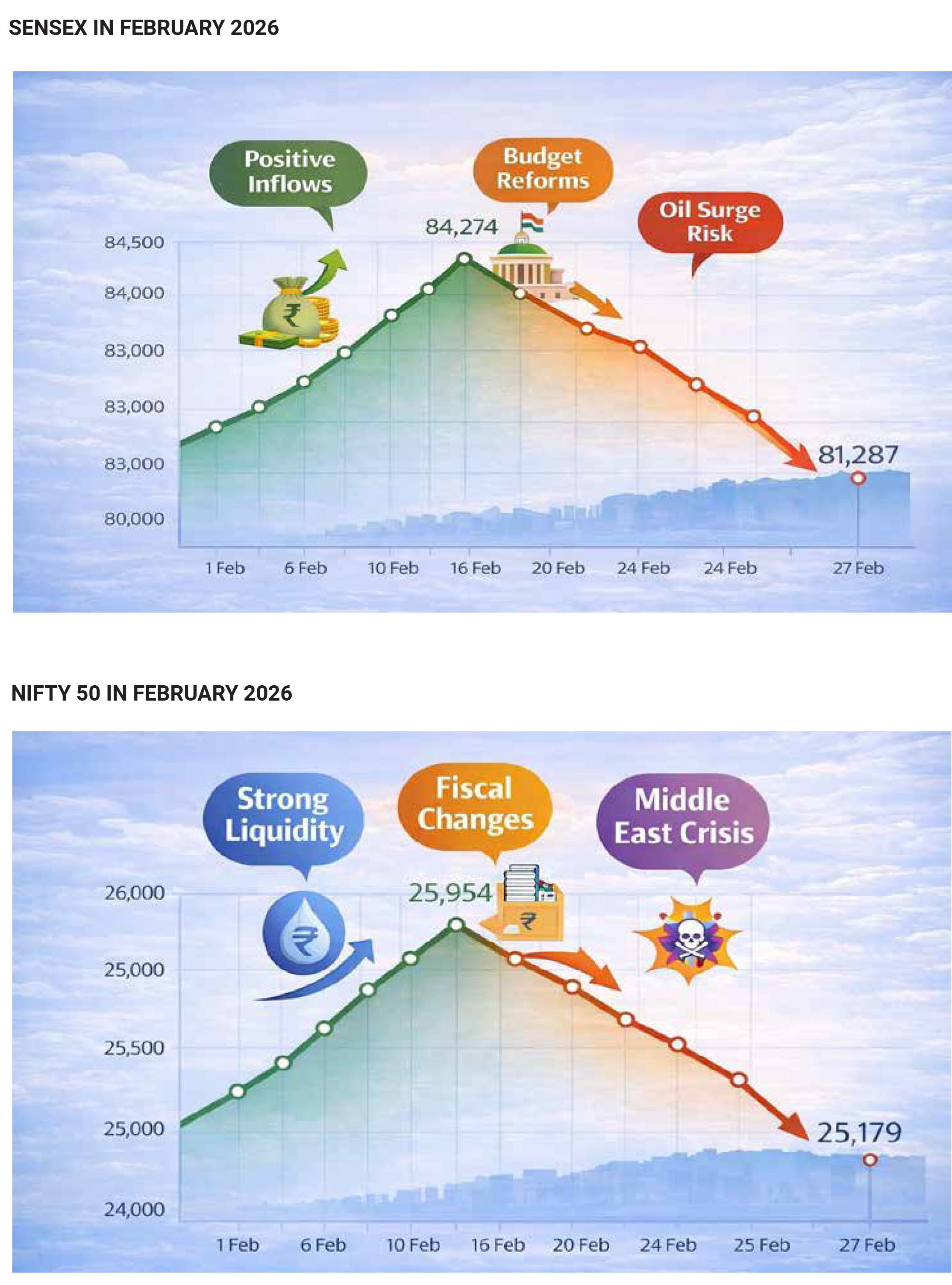

February 2026 proved to be a month of sharp

cross-currents for Indian equity markets. After an early

surge and multiple volatility spikes, the Sensex closed

the month with a modest decline of roughly 1–1.3%.

While the headline number suggests a mild pullback, the

internal churn beneath the surface was far more

dramatic, driven by sector-specific shocks, policy

surprises, shifting foreign flows, and global macro

tensions.

The benchmark began February on a strong footing,

buoyed by improved risk sentiment and renewed buying

interest. On 1 February, the index settled at 81,666.46

after a sharp jump, reflecting optimism around domestic

growth cues and foreign investor participation. However,

momentum soon tapered. Through mid-February, the

market traded in a tight consolidation band. By the week

ended 20 February, the Sensex had managed a marginal

weekly gain of just 0.23%, closing near 82,814.7. This

stability masked growing stress within certain

heavyweight sectors. By 27 February, the index had

drifted back toward the 81,300 zone, turning the month

marginally negative. On a calendar-year basis, the

Sensex was down about 2.8% by mid-month, reflecting

corrective pressure after the early January peak near

85,762. Despite February’s dip, the index remained

roughly 11% higher than a year earlier. The broader

12-month uptrend was intact. What February

represented was less a structural breakdown and more a

consolidation phase within a longer-term positive

trajectory.

The defining feature of February was the brutal selloff in

technology stocks. The NIFTY IT index plunged nearly

19.5% during the month — its steepest fall since the 2008

global financial crisis. Approximately ₹5.7 trillion in IT

market capitalisation was erased. Heavyweights faced

aggressive derating as concerns mounted that rapid AI

automation in the United States could disrupt traditional

Indian outsourcing models. Large exporters were hit

hardest, amplifying intraday swings in the broader

benchmarks given their significant index weights. The

market began reassessing growth visibility, pricing

power, and long-term competitive positioning for Indian

IT majors in an AI-driven global landscape

The second volatility catalyst came from the Union

Budget 2026, presented on 1 February. While the Budget

was growth-oriented in its macro framing, markets

reacted sharply to changes in derivatives taxation. The

Securities Transaction Tax (STT) on futures was raised

by approximately 150%, and on options by around 50%,

materially increasing trading costs. On Budget Day, the

Sensex plunged nearly 2% intraday, falling over

2,300–2,400 points from its peak and wiping out an

estimated ₹10–11 lakh crore in investor wealth in a

single session. The India VIX jumped roughly 11%,

reflecting an abrupt repricing of risk. Higher derivatives

costs triggered aggressive unwinding in index and stock

futures. Liquidity thinned temporarily as algorithmic and

high-frequency traders recalibrated positions. Brokerage

and capital-market-linked stocks saw sharp declines on

fears of lower F&O volumes and revenue pressure.

One of the most significant undercurrents in February

was the dramatic reversal in foreign portfolio investor

(FPI) flows. After three months of heavy selling — with

outflows of over ₹62,000 crore between November and

January — foreign investors turned decisive net buyers.

In February alone, FPIs infused approximately ₹22,615

crore into Indian equities, the strongest monthly equity

inflow in around 17 months. Including debt, total FPI

inflows crossed ₹31,000 crore. The shift was driven by

several factors: a growth-oriented fiscal stance, an

interim India–US trade agreement reducing tariff

overhang, softer-than-expected US inflation, improved

Q3 FY26 earnings growth of roughly 14.7% and lastly

valuation corrections after the late-2025 selloff.

However, flows were not uniform. While financials and

capital goods attracted buying, IT continued to see heavy

foreign selling — roughly ₹10,956 crore in February alone.

The message was clear: foreign capital was rotating, not

retreating.

Beyond domestic factors, global uncertainties added to

volatility. Rising tensions surrounding a US ultimatum to

Iran pushed oil prices above $70 per barrel, lifting the

equity risk premium. Late in the month, selling pressure

spread to private sector banks. Heavyweights such as

ICICI Bank, Kotak Mahindra Bank, and HDFC Bank

contributed significantly to a large single-day drop on 26

February. Given their combined weight in the index, even

moderate declines in these stocks amplified benchmark

weakness. At least five sessions during the month

recorded declines exceeding 1, underscoring the

elevated day-to-day swings.

Despite the noise, the structural underpinnings of the

market remained constructive. Earnings growth was

intact. Domestic macro indicators were stable. Capital

expenditure momentum continued. Foreign investors

returned selectively. February 2026 ultimately illustrated

a market transitioning from momentum-driven euphoria

to a more discriminating, fundamentals-driven phase.

The IT rout forced valuation recalibration. The

Budget-induced derivatives change reshaped trading

dynamics. Global tensions injected episodic risk

aversion. Yet capital did not flee — it rotated.

For market players, the key takeaway is that February’s

decline was not a systemic breakdown but a corrective

consolidation within a broader uptrend. With valuations

reset in select sectors and foreign flows stabilising, the

month may well be remembered as a volatility shock that

strengthened market structure rather than weakened it.

In equity markets, periods of discomfort often lay the

groundwork for more sustainable advances. February

2026 was one such chapter.

Indian debt markets navigated February 2026 with

resilience, delivering stable to slightly positive returns

despite heavy event risk. The month began with the

Union Budget 2026, which set the tone for bond trading

by combining record borrowing numbers with a

reaffirmed fiscal consolidation path. While the headline

borrowing figure initially made participants cautious, the

broader macro and policy signals helped benchmark

yields remain range-bound and slightly softer over the

month.

The Budget projected gross central government market

borrowing of approximately ₹17.2 lakh crore for FY27 —

higher than many dealers had pencilled in. This

immediately raised concerns about supply–demand

balance in government securities (G-secs). Elevated

issuance, alongside substantial state government

borrowing, suggested that rupee bonds could face

upward pressure on yields as the market absorbed the

borrowing calendar. However, the fiscal messaging was

equally important. The government reiterated a fiscal

deficit target of 4.3% of GDP for FY27, continuing gradual

consolidation from 4.4% in FY26 and signalling intent to

lower the debt-to-GDP ratio toward the mid-50% range

over time. This combination — near-term supply pressure

but credible fiscal glide path — produced a nuanced

reaction. Long-duration bonds faced mild bearish bias

due to heavier issuance expectations, but sovereign risk

perception remained contained. Term premia did not

expand sharply because markets interpreted the

borrowing within a disciplined macro framework rather

than fiscal slippage. Beyond headline borrowing, the

Budget also introduced structural measures aimed at

deepening the bond market. Proposals included a

market-making framework for corporate bonds,

derivatives on corporate bond indices, and total return

swaps to enhance liquidity and price discovery. While

these reforms did not immediately alter February pricing,

they reinforced the longer-term institutionalisation of

India’s debt markets, potentially supporting spreads and

attracting broader participation over time.

Shortly after the Budget, attention shifted to the February

monetary policy decision by the Reserve Bank of India.

The Monetary Policy Committee kept the repo rate

unchanged at 5.25% and retained a neutral stance,

signalling that the rate-cutting cycle — which had

delivered roughly 125 basis points of easing since early

2025 — had transitioned into a “hold and watch” phase.

The RBI underscored benign inflation, with CPI projected

around 4–4.2% in early FY27, alongside robust real GDP

growth expectations near 7%+. On policy day, bonds

initially sold off. The 10-year yield rose roughly 9 basis

points to about 6.74%, reflecting disappointment that the

RBI did not announce fresh bond purchases or additional

liquidity-boosting measures to offset the large

government borrowing programme. Traders had hoped

for explicit support through open market operations

(OMOs), especially given record issuance projections.

The absence of such measures triggered a brief tactical

rise in yields.

Yet this reaction proved temporary. By anchoring the

repo rate at 5.25%, maintaining the Standing Deposit

Facility (SDF) at 5.00% and the MSF/Bank Rate at 5.50%,

and signalling comfort with surplus system liquidity, the

RBI effectively stabilised expectations at the short end of

the curve. Liquidity remained ample, supported by prior

OMOs and FX swap operations amounting to several

lakh crore rupees. The message was clear: policy rates

were likely at or near the peak for this cycle, and macro

conditions were stable. This limited downside for bond

prices after the initial selloff.

As the month progressed, the 10-year benchmark yield

moved mostly within a tight 6.65–6.75% band, signalling

a stable to slightly firmer bond market even as equity

markets experienced sharp volatility. By 2 March 2026,

the 10-year G-sec yield stood near 6.70%, roughly 3 basis

points lower than a month earlier. This modest easing

translated into small price gains for benchmark bonds in

February — a respectable performance given the heavy

issuance backdrop and global uncertainties.

Foreign portfolio investor (FPI) behaviour provided

another layer of support. February saw consistent net

buying in Indian debt. In one weekly reading alone, FPIs

added approximately ₹5,139 crore to debt — among the

strongest weekly tallies in the current phase. Flow

analysis suggested that debt, rather than equities, was

the main driver of net foreign inflows during the month.

NSDL-based commentary repeatedly described “another

week of positive debt flows,” highlighting improving

foreign participation after earlier volatility. Several

structural factors underpin this foreign appetite. India’s

entry into major global bond indices has steadily

increased its visibility and weight in global fixed-income

portfolios. Additionally, relatively high real yields compared

to many emerging and developed peers make Indian G-secs

attractive in a world where inflation pressures are easing but

nominal yields remain compressed elsewhere. February’s

pattern — stable to slightly lower yields combined with solid

FPI buying — fits the broader narrative of gradual rerating,

where global investors use volatility episodes to build

structural positions.

Macro fundamentals stayed strong in early 2026, with real

GDP growth projected at 6.8–7.2%, contained inflation,

disciplined fiscal policy, and stable currency. Robust bond

auction participation demonstrated solid demand for rupee

debt. March saw yields edge higher due to technical supply

factors, not weakening fundamentals, highlighting

continued investor confidence in Indian debt markets.

Segment-wise, the implications were differentiated.

Long-duration and gilt funds experienced intermittent

volatility due to supply sensitivity and long-end yield

movements. In contrast, short-duration and corporate bond

funds benefited from stable short-term rates and attractive

carry. Anchored policy corridor rates helped money market

instruments and short-duration strategies deliver relatively

steady returns through the month.

In summary, February 2026 was a test of balance for Indian

debt markets. The Union Budget introduced record

borrowing numbers that initially unsettled sentiment, while

the RBI’s decision to hold rates without fresh bond

purchases caused a brief tactical spike in yields. Yet strong

macro fundamentals, credible fiscal consolidation, surplus

liquidity, healthy auction demand, and sustained FPI inflows

ensured that yields remained contained. The benchmark

10-year yield ended the month marginally lower, and debt

delivered modest gains. Rather than succumbing to supply

fears, the bond market demonstrated maturity and

structural depth. February’s performance underscored a key

theme for 2026: India’s debt market is increasingly

supported by institutional credibility, global integration, and

disciplined macro management — factors that together

helped it weather event-driven volatility and emerge

reasonably stronger.

February 2026 was one of the most turbulent months for

Indian bullion in recent memory, with the Union Budget 2026

acting as the immediate catalyst for extreme price swings.

The volatility was most visible on Budget Day, when both

gold and silver futures on MCX crashed sharply in intraday

trade before staging partial recoveries. While the broader

global backdrop contributed to the turbulence, the Budget’s

tax changes — particularly around Sovereign Gold Bonds

(SGBs) — triggered aggressive liquidation in leveraged

and “paper gold” positions, setting off a chain reaction

across bullion markets.

The key Budget announcement that unsettled the bullion

trade was the removal of capital gains tax exemption at

maturity for secondary-market buyers of Sovereign Gold

Bonds. Going forward, tax-free status would apply only to

original subscribers holding bonds until redemption. This

reduced the relative attractiveness of SGBs as a

tax-efficient alternative to physical gold and gold ETFs.

The move sparked profit booking in gold-linked financial

products and amplified selling pressure in futures, where

leveraged positions unwound rapidly.

On 1 February, MCX gold futures crashed over ₹10,000

per 10 grams and silver even more sharply amid record

pre-Budget highs, as policy surprises triggered a

technical selloff. Hopes for import duty reductions were

dashed, keeping gold and silver taxes unchanged, which

further hurt sentiment. However, this panic was brief. As

the month progressed, safe-haven demand and steadier

global markets supported a sharp recovery. By February’s

end, gold staged a V-shaped rebound, closing near

₹1,61,720 per 10 grams, with Delhi 24K gold up 0.6% for

the month, demonstrating buyers’ willingness to

accumulate on dips.

Silver, however, told a far more dramatic story. Spot

prices in India swung wildly, beginning near ₹3,50,000 per

kg on 1 February, collapsing to around ₹2,55,000 by 18

February, and then rebounding toward

₹2,85,000–3,00,000 per kg before consolidating into

month-end. The boom-bust-rebound pattern reflected

silver’s inherently higher beta nature. In corrections, silver

typically moves two to three times as much as gold, and

February followed that script precisely.

Silver’s sharper decline compared to gold in February

2026 was driven by several factors. Silver had seen an

outsized rally, with prices multiplying over the past two

years, resulting in stretched technicals and heavy

speculative positions fuelled by AI-related industrial

demand, supply concerns in China, and robust ETF

inflows. When global precious metals corrected amid a

stronger US dollar and expectations of prolonged high

interest rates, silver led the sell-off. The SGB tax change

impacted both gold and silver, but thinner liquidity and

high futures open interest in silver accelerated margin

calls and forced selling, amplifying volatility. Gold,

meanwhile, held up better due to consistent safe-haven

demand as geopolitical tensions and equity volatility

increased. By late February, both metals stabilised. Gold

entered mild profit-taking near monthly highs, while silver

consolidated around ₹2,80,000–2,85,000 per kg, with

uniform pricing across cities reflecting reduced panic and

cleaner positioning.

In summary, February 2026 was defined by a

Budget-triggered shock that exposed overstretched

positioning in bullion, particularly silver. Gold endured a

sharp early fall but recovered to post a small net monthly

gain, reinforcing its role as a resilient hedge. Silver, by

contrast, experienced a violent boom-bust-rebound cycle,

reflecting its higher beta and speculative character.

Together, the two metals illustrated how policy surprises,

technical positioning, and global macro forces can converge

to produce extreme but ultimately self-correcting volatility in

commodity markets.

The Indian Rupee (INR) depreciated moderately against the

US Dollar (USD) in February 2026, weakening by around

0.5–1.3%. USD/INR started the month near 90.70–90.75

and gradually rose, reaching 91.30–91.59 by early March.

This decline was measured, staying well below January’s

peak of 92.29, and reflected a controlled adjustment rather

than abrupt volatility. The weakening rupee was primarily

driven by global dollar strength. The US dollar index (DXY)

firmed as the Federal Reserve adopted a cautious

“higher-for-longer” rate outlook, with fewer expected cuts in

2026. Elevated US real yields and speculation about a more

hawkish policy stance further bolstered the dollar.

Consequently, emerging market currencies including the

rupee faced sustained external pressure. Despite

intermittent foreign inflows that provided brief support, the

overall trend was towards gradual depreciation, highlighting

how global monetary policy shifts and strong US yields

shape currency movements in India.

Domestically, the Union Budget 2026 added another layer of

caution. The government’s announcement of record gross

market borrowing of around ₹17.2 trillion for FY27 triggered

concerns about fiscal supply, current account pressures,

and sustained dollar demand from importers. While the

Budget reaffirmed fiscal consolidation targets, the scale of

borrowing heightened expectations of continued foreign

currency demand, particularly from oil marketing companies

and large importers hedging exposures. With crude oil

trading above $70 per barrel for much of the month,

India’s oil import bill remained elevated, structurally

increasing dollar demand in the domestic forex market.

Foreign portfolio investor (FPI) flows presented a mixed

dynamic. Although FPIs were net buyers of Indian

equities to the tune of roughly ₹22,000 crore during

February, overall forex demand remained tilted toward

the dollar. Debt inflows, oil-related payments, and

safe-haven positioning amid Middle East geopolitical

tensions kept underlying USD demand firm. Additionally,

higher US yields marginally reduced the relative carry

attractiveness of rupee-denominated assets, even

though the Reserve Bank of India’s repo rate stood at

5.25%. This dynamic limited the positive impact that

equity inflows might otherwise have had on the currency.

Stabilising forces, however, were equally important in

containing the rupee’s downside. The Reserve Bank of

India maintained a steady monetary policy stance in

February, keeping the repo rate unchanged at 5.25% and

signalling liquidity comfort. System liquidity remained in

surplus, anchoring short-term rates and supporting

investor confidence in macro stability. Market

participants widely believe that the RBI conducted

calibrated interventions in both spot and non-deliverable

forward (NDF) markets — potentially in the range of

$5–10 billion — to prevent excessive volatility. These

actions appeared effective in defending the 91.50–92.00

zone, ensuring that depreciation remained gradual and

contained rather than abrupt.

As a result, USD/INR traded within a relatively tight

monthly range of approximately 90.65–91.60, a notable

contrast to the sharper swings observed in equity and

commodity markets during the same period. Compared

to several Asian peers such as the Korean won or

Indonesian rupiah, the rupee demonstrated relative

resilience, reflecting India’s stronger macro

fundamentals, steady growth outlook, and proactive

central bank management. In essence, February 2026

was characterised not by rupee instability, but by

controlled depreciation shaped by global dollar strength,

fiscal supply optics, and oil dynamics — offset by credible

policy and vigilant intervention that kept currency

volatility firmly in check.

In February 2026, crude oil markets were dominated by a

Reserve contributed to a more cautious risk environment

in financial markets, amplifying volatility across equities

and fixed income.

For India, the crude price surge carried particular

importance given the country’s heavy reliance on

imported oil. A sustained climb toward $78 per barrel

from sub-$70 levels translated into higher import bills,

pressure on the current account deficit, and incremental

inflationary pressure on fuel and transportation costs. As

Brent remained elevated, many Indian refiners and oil

marketing companies faced margin compression on the

downstream side even as upstream producers saw

improved realisations.

In summary, February 2026’s crude oil price action was

dominated by a complex interplay between geopolitical

risk and market positioning. Fear of disrupted supplies

through strategically vital routes like the Strait of Hormuz,

coupled with an ongoing conflict environment, pushed

prices significantly higher over the month. Attempts by

OPEC+ to bolster production and sporadic diplomatic

optimism offered limited relief, but they were not enough

to counter the dominant narrative of supply risk. Brent’s

march toward the high $70s illustrated how geopolitical

catalysts can override fundamental supply and demand

considerations in the short term, embedding a

pronounced risk premium that reverberated through

commodity, currency, and equity markets alike.

On 26 February 2026, the Securities and Exchange Board

of India (SEBI) unveiled a landmark reform of mutual fund

categorization—reshaping an ₹81 lakh crore industry with

sharper definitions, tighter risk controls, and a brand-new

product category. At the heart of the overhaul is

simplification. Schemes are now consolidated into five

broad buckets: Equity-Oriented, Debt-Oriented, Hybrid,

Life Cycle Funds (new), and Other Schemes (Index Funds,

ETFs, and Fund of Funds). In a major shift,

solution-oriented schemes such as retirement and

children’s funds have been discontinued for fresh inflows

and will merge into comparable categories with

unitholder approval.

Equity schemes face stricter norms. Dividend Yield,

Value, Contra, and Focused funds must now hold a

minimum 80% in equities—up from 65%—ensuring

clearer “true-to-label” positioning. The remaining

allocation can include gold and silver ETFs, REITs, and

InvITs, offering measured diversification. Hybrid funds

have also been precisely defined, from Conservative

Hybrid (10–25% equity) to Aggressive Hybrid (65–80%),

while Multi-Asset funds must allocate at least 10% each

across three asset classes.

Perhaps the most significant structural reform is the 50%

portfolio overlap cap within the same fund house. Value

and Contra funds cannot mirror each other beyond this

threshold, and sectoral/thematic funds must reduce

overlap with other equity schemes in phased compliance

over three years. Monthly public disclosures will further

enhance transparency.

The headline innovation is the introduction of Life Cycle

Funds—open-ended schemes with fixed tenures (5–30

years) and automatic glide paths. These funds begin

equity-heavy and gradually shift toward debt as maturity

approaches, aligning risk with investors’ life stages. With

graded exit loads and disciplined asset transitions, they

aim to reduce emotional investing and simplify

long-term planning.

Implementation begins immediately, with phased

compliance through 2029—marking one of the most

comprehensive mutual fund reforms in recent years.