Topic 1: EQUITY: SWIVELLING EFFECT

February 2026 proved to be a month of sharp

cross-currents for Indian equity markets. After an early

surge and multiple volatility spikes, the Sensex closed

the month with a modest decline of roughly 1–1.3%.

While the headline number suggests a mild pullback, the

internal churn beneath the surface was far more

dramatic, driven by sector-specific shocks, policy

surprises, shifting foreign flows, and global macro

tensions.

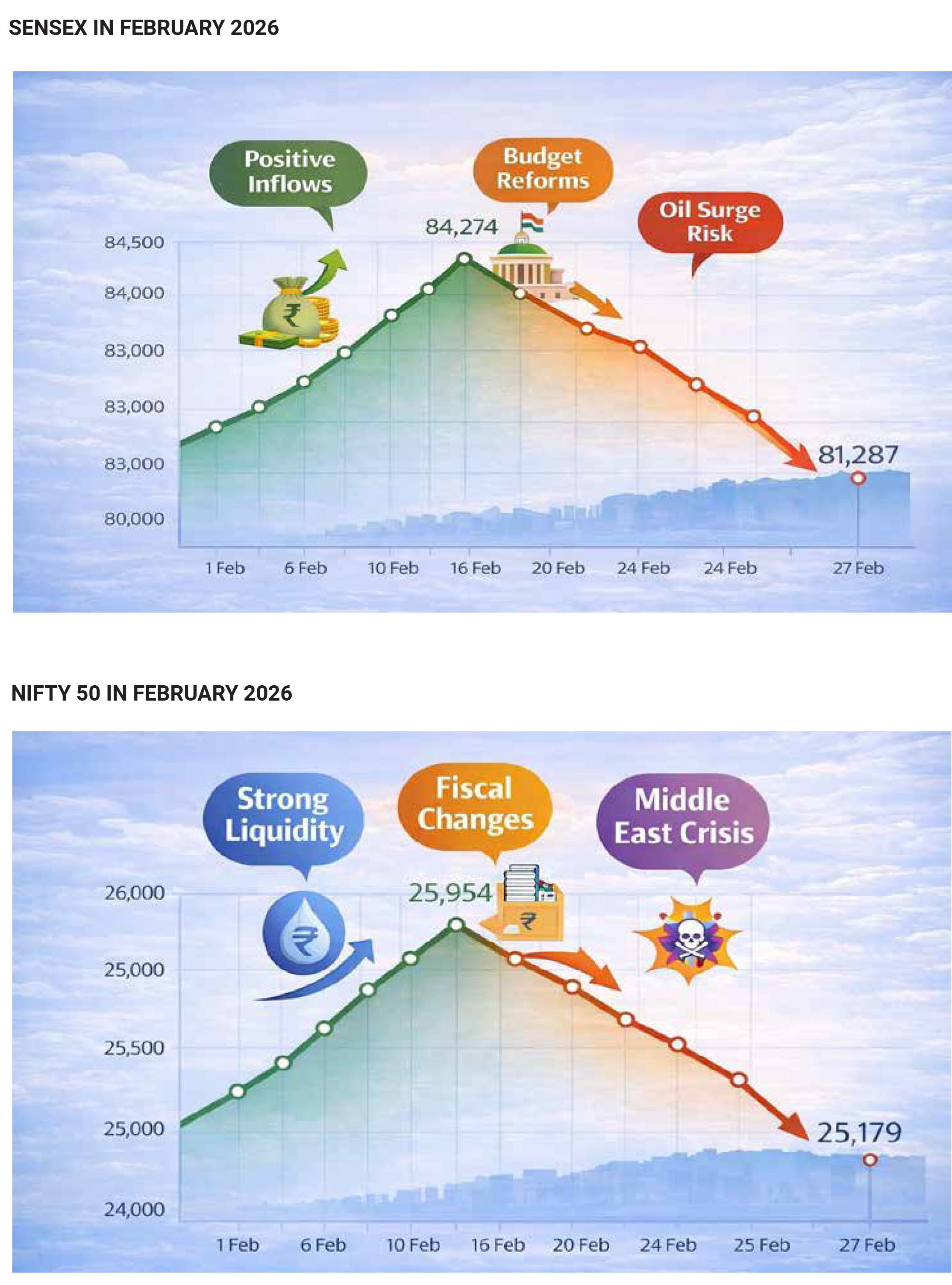

The benchmark began February on a strong footing,

buoyed by improved risk sentiment and renewed buying

interest. On 1 February, the index settled at 81,666.46

after a sharp jump, reflecting optimism around domestic

growth cues and foreign investor participation. However,

momentum soon tapered. Through mid-February, the

market traded in a tight consolidation band. By the week

ended 20 February, the Sensex had managed a marginal

weekly gain of just 0.23%, closing near 82,814.7. This

stability masked growing stress within certain

heavyweight sectors. By 27 February, the index had

drifted back toward the 81,300 zone, turning the month

marginally negative. On a calendar-year basis, the

Sensex was down about 2.8% by mid-month, reflecting

corrective pressure after the early January peak near

85,762. Despite February’s dip, the index remained

roughly 11% higher than a year earlier. The broader

12-month uptrend was intact. What February

represented was less a structural breakdown and more a

consolidation phase within a longer-term positive

trajectory.

The defining feature of February was the brutal selloff in

technology stocks. The NIFTY IT index plunged nearly

19.5% during the month — its steepest fall since the 2008

global financial crisis. Approximately ₹5.7 trillion in IT

market capitalisation was erased. Heavyweights faced

aggressive derating as concerns mounted that rapid AI

automation in the United States could disrupt traditional

Indian outsourcing models. Large exporters were hit

hardest, amplifying intraday swings in the broader

benchmarks given their significant index weights. The

market began reassessing growth visibility, pricing

power, and long-term competitive positioning for Indian

IT majors in an AI-driven global landscape

The second volatility catalyst came from the Union

Budget 2026, presented on 1 February. While the Budget

was growth-oriented in its macro framing, markets

reacted sharply to changes in derivatives taxation. The

Securities Transaction Tax (STT) on futures was raised

by approximately 150%, and on options by around 50%,

materially increasing trading costs. On Budget Day, the

Sensex plunged nearly 2% intraday, falling over

2,300–2,400 points from its peak and wiping out an

estimated ₹10–11 lakh crore in investor wealth in a

single session. The India VIX jumped roughly 11%,

reflecting an abrupt repricing of risk. Higher derivatives

costs triggered aggressive unwinding in index and stock

futures. Liquidity thinned temporarily as algorithmic and

high-frequency traders recalibrated positions. Brokerage

and capital-market-linked stocks saw sharp declines on

fears of lower F&O volumes and revenue pressure.

One of the most significant undercurrents in February

was the dramatic reversal in foreign portfolio investor

(FPI) flows. After three months of heavy selling — with

outflows of over ₹62,000 crore between November and

January — foreign investors turned decisive net buyers.

In February alone, FPIs infused approximately ₹22,615

crore into Indian equities, the strongest monthly equity

inflow in around 17 months. Including debt, total FPI

inflows crossed ₹31,000 crore. The shift was driven by

several factors: a growth-oriented fiscal stance, an

interim India–US trade agreement reducing tariff

overhang, softer-than-expected US inflation, improved

Q3 FY26 earnings growth of roughly 14.7% and lastly

valuation corrections after the late-2025 selloff.

However, flows were not uniform. While financials and

capital goods attracted buying, IT continued to see heavy

foreign selling — roughly ₹10,956 crore in February alone.

The message was clear: foreign capital was rotating, not

retreating.

Beyond domestic factors, global uncertainties added to

volatility. Rising tensions surrounding a US ultimatum to

Iran pushed oil prices above $70 per barrel, lifting the

equity risk premium. Late in the month, selling pressure

spread to private sector banks. Heavyweights such as

ICICI Bank, Kotak Mahindra Bank, and HDFC Bank

contributed significantly to a large single-day drop on 26

February. Given their combined weight in the index, even

moderate declines in these stocks amplified benchmark

weakness. At least five sessions during the month

recorded declines exceeding 1, underscoring the

elevated day-to-day swings.

Despite the noise, the structural underpinnings of the

market remained constructive. Earnings growth was

intact. Domestic macro indicators were stable. Capital

expenditure momentum continued. Foreign investors

returned selectively. February 2026 ultimately illustrated

a market transitioning from momentum-driven euphoria

to a more discriminating, fundamentals-driven phase.

The IT rout forced valuation recalibration. The

Budget-induced derivatives change reshaped trading

dynamics. Global tensions injected episodic risk

aversion. Yet capital did not flee — it rotated.

For market players, the key takeaway is that February’s

decline was not a systemic breakdown but a corrective

consolidation within a broader uptrend. With valuations

reset in select sectors and foreign flows stabilising, the

month may well be remembered as a volatility shock that

strengthened market structure rather than weakened it.

In equity markets, periods of discomfort often lay the

groundwork for more sustainable advances. February

2026 was one such chapter.