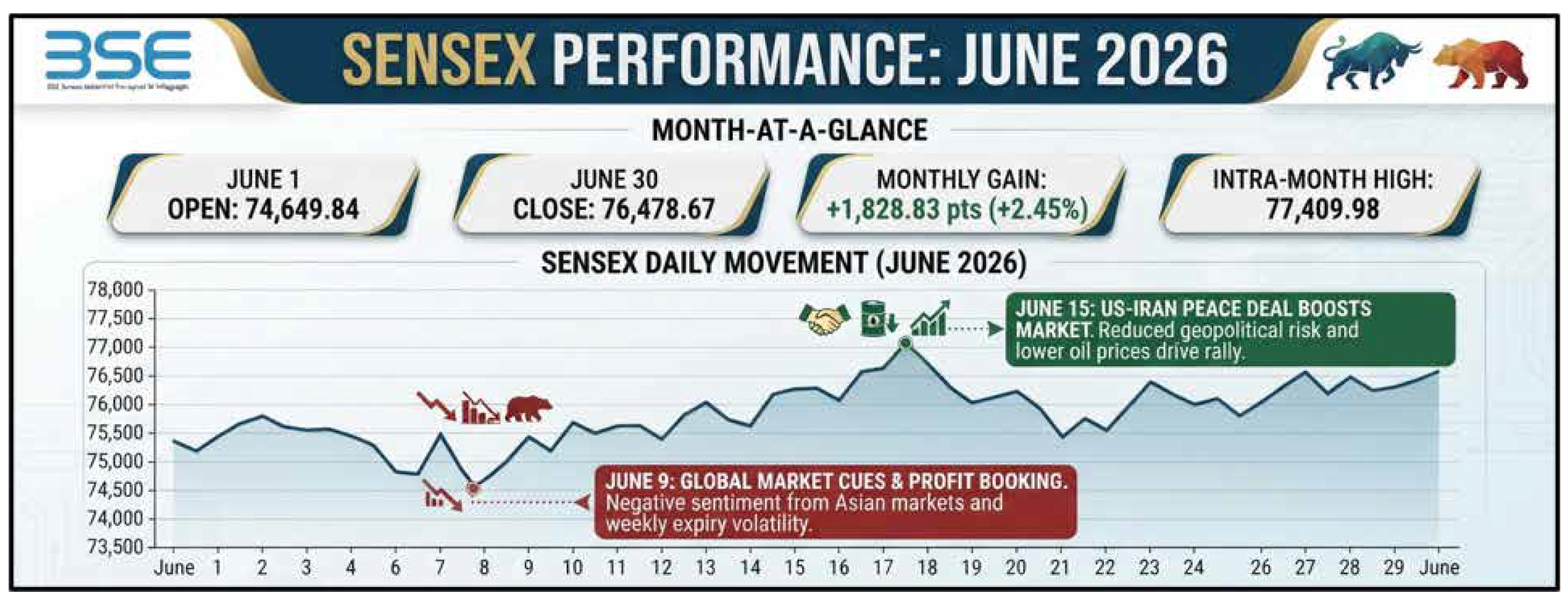

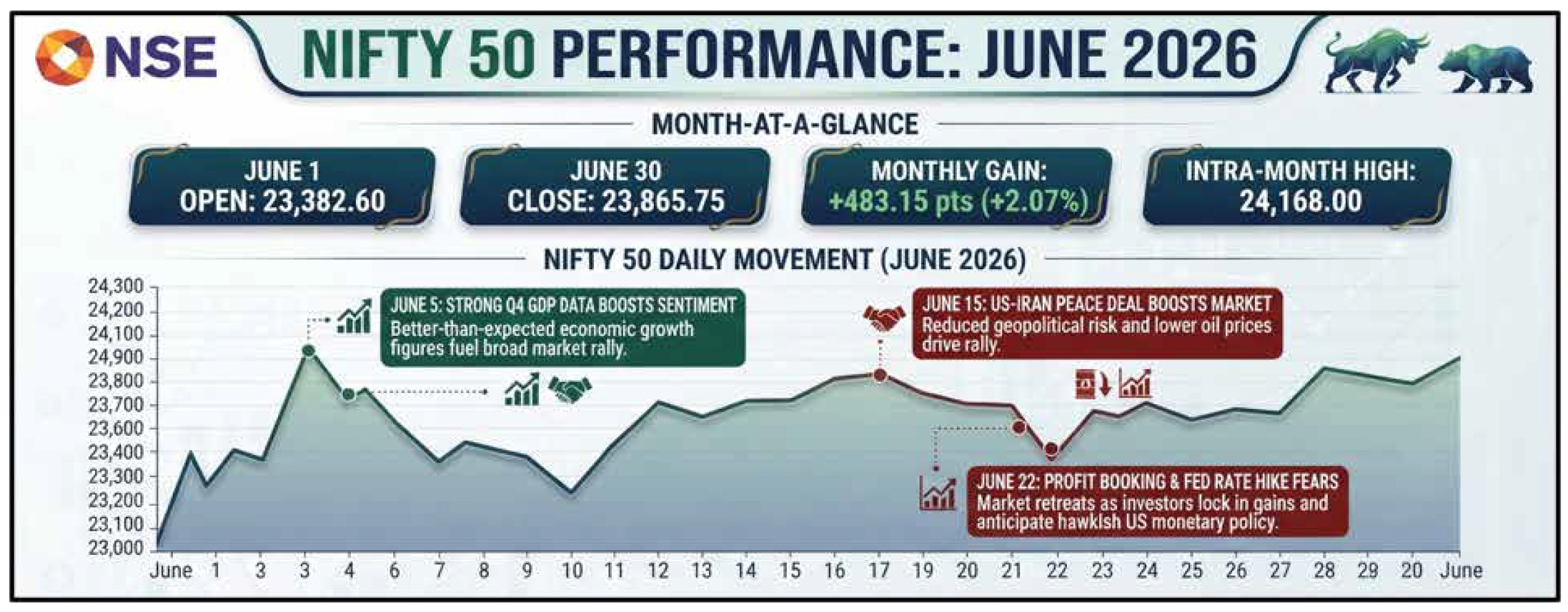

India's equity markets ended June 2026 on a positive note despite experiencing one of the most volatile months of the year. The BSE Sensex closed at 76,478.67, gaining 1,702.93 points (2.28%), while the NSE Nifty 50 finished at 23,865.75, up 483.15 points (2.07%). Although the benchmark indices posted modest gains, the broader market displayed greater resilience, with mid- and small-cap stocks outperforming large caps as domestic investors increasingly favored higher-beta, India-focused companies. Throughout the month, markets were influenced by a complex mix of domestic monetary policy, geopolitical developments in West Asia, global risk sentiment, and contrasting institutional investment flows. The month began with the Reserve Bank of India keeping the repo rate unchanged at 5.25%, but the accompanying downgrade in FY27 GDP growth projections and upward revision to inflation expectations reinforced a "higher-for-longer" interest rate outlook, tempering investor optimism. Geopolitical tensions soon became the dominant market driver. Escalating conflict between Israel and Iran, including military strikes and fears of disruption around the Strait of Hormuz, pushed crude oil prices close to US$100 per barrel during the first week of June. The resulting spike in oil prices triggered a sharp sell-off in Indian equities on 5 June, with the Sensex and Nifty falling around 1% to multi-month lows. A temporary easing of hostilities over the following days allowed

crude prices to retreat, enabling Indian markets to recover, led by banking and broader market stocks. Fresh concerns emerged around 10 June, when the United States expanded military operations against Iranian targets, reviving fears of a wider regional conflict. However, sentiment improved during the second half of the month as reports of a potential US-Iran ceasefire and diplomatic negotiations reduced concerns over prolonged disruptions to global energy supplies. Markets responded positively to these developments, although intermittent reports of ceasefire violations and tensions around the Strait of Hormuz continued to create bouts of volatility. Another major setback occurred on 23 June, when a global risk-off wave coinciding with weekly options expiry and an unexpected double-digit decline in South Korea's KOSPI index triggered widespread selling across Asian markets, including India. Defensive sectors such as pharmaceuticals outperformed during this period as investors sought safer assets. Renewed US military strikes on Iranian missile and radar installations later in the month generated only a muted market reaction, indicating that investors had begun pricing in recurring geopolitical flare-ups rather than anticipating a full-scale regional conflict. Nevertheless, profit booking in the final trading sessions, particularly in technology stocks, resulted in modest declines on the last day of June. Sectoral performance reflected significant rotation within the market. Banking was the strongest performer, with the BSE Bankex rising 6.38%, supported by expectations of stable interest rates, improving credit growth, and stronger earnings visibility. Realty stocks also gained 5.86%, benefiting from supportive financing conditions and resilient housing demand. In contrast, metals emerged as the weakest sector, declining 8.15% amid global growth concerns and volatile commodity prices. Technology stocks also underperformed, with the BSE Teck Index falling 5.84%, as investors remained concerned about slowing global IT spending, elevated valuations, and the long-term impact of artificial intelligence on traditional outsourcing business models. Auto and PSU banking stocks witnessed mixed performance towards the month-end as leadership continued rotating across sectors. One of the defining characteristics of June was the stark divergence between foreign and domestic institutional investors. Foreign Institutional Investors (FIIs) remained persistent sellers, recording their twelfth consecutive month of net outflows with approximately ₹49,028 crore withdrawn from Indian equities due to concerns over US interest rates, currency movements, and global asset allocation. In contrast, Domestic Institutional Investors (DIIs) invested around ₹85,800 crore, supported by strong mutual fund SIP inflows, insurance companies, pension funds, and other long-term domestic investors. This consistent domestic buying repeatedly cushioned the market against foreign selling and external shocks, demonstrating the growing maturity and resilience of India's capital markets. Even on the final trading day of the month, DIIs significantly outpaced FII selling, reinforcing domestic liquidity as the primary support for equities. Overall, June 2026 highlighted the increasing ability of Indian markets to absorb external geopolitical risks, tighter monetary conditions, and global volatility while still delivering positive monthly returns. The combination of strong domestic participation, sectoral rotation, resilient banking stocks, and sustained retail inflows enabled Indian equities to withstand repeated bouts of uncertainty, reinforcing confidence in the long-term structural strength of the market despite a challenging global environment.

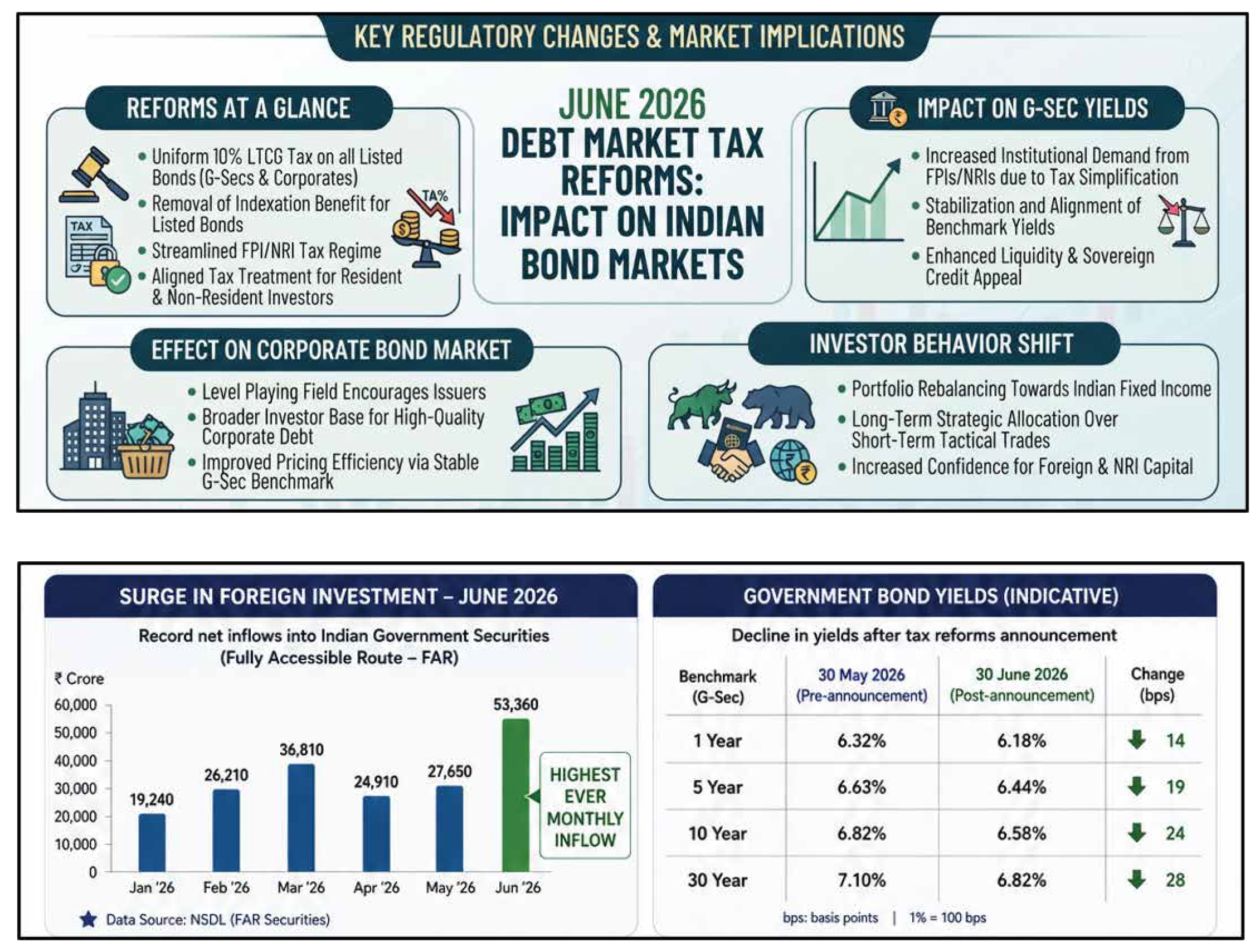

India's debt markets turned in a strikingly strong performance in June 2026, standing in sharp contrast to the choppier mood in equities that month. The headline move was in government securities, where the 10-year benchmark yield slid from around 7.02 percent at the end of May to roughly 6.75-6.77 percent by late June, a meaningful drop driven by a wave of record foreign inflows and a retreat in crude oil prices that improved both the inflation outlook and the rupee's standing. This wasn't confined to the long end of the curve either — the money market, which had been under real stress in May, normalized considerably. With the Reserve Bank of India holding its repo rate steady at 5.25 percent and liquidity conditions easing, certificate of deposit yields fell sharply, dropping around 60 basis points to settle near 7.0 percent. Perhaps more tellingly, the front end of the yield curve, which had been unusually inverted — with very short-tenor instruments yielding more than 1-3 year paper — began to unwind, restoring a more conventional upward-sloping term structure. Corporate bonds joined the rally too, buoyed by improved liquidity and firm demand at the higher-rated end of the market, with primary issuance picking up and spreads holding relatively tight at around 500 basis points for the broader market, even though episodic risk-off days tied to tensions in West Asia kept investors somewhat selective about where they deployed capital. The single biggest force behind this rally was the behavior of foreign investors, who poured money into Indian debt at a scale rarely seen before. Foreign portfolio investors funneled a record amount into the market during June — figures vary slightly depending on the source, with some accounts citing approximately ₹53,300 crore with the bulk of that capital flowing into government bonds and treasury bills through the Fully Accessible Route and other general investment limits. This wall of debt inflows was significant enough to substantially offset heavy foreign selling in equities that same month, and by some measures it pushed India's overall net FII flow for June into slightly positive territory despite the well-documented exodus from stocks. Falling oil prices reinforced the trend from a different angle: crude retreated from levels near $100 a barrel earlier in the month to the low $80s by its end, which eased both inflation worries and current-account concerns, giving yields room to grind lower even as geopolitical headlines continued to surface periodically. Behind this surge in foreign appetite was a deliberate and fairly dramatic policy intervention by the Indian government. Through the Income-tax (Amendment) Ordinance, 2026, promulgated in early June with retrospective effect from April 1, 2026, authorities eliminated a set of tax burdens that had long made Indian sovereign debt less competitive relative to other emerging markets. The changes were substantial: the withholding tax on interest income, previously 20 percent, was reduced to zero; long-term capital gains tax, previously 12.5 percent, was eliminated entirely; and short-term capital gains tax, which could run as high as 30 percent, was likewise fully exempted. Importantly, these exemptions were narrowly targeted — they apply specifically to investments in government securities, including the expanded Fully Accessible Route tenors and Sovereign Green Bonds, but do not extend to corporate bonds, non-convertible debentures, or investments made by resident Indian citizens. Alongside the tax overhaul, the RBI also expanded the range of tenors eligible under the Fully Accessible Route, adding another layer of accessibility for foreign capital. The single biggest force behind this rally was the behavior of foreign investors, who poured money into Indian debt at a scale rarely seen before. Foreign portfolio investors funneled a record amount into the market during June — figures vary slightly depending on the source, with some accounts citing approximately ₹53,300 crore with the bulk of that capital flowing into government bonds and treasury bills through the Fully Accessible Route and other general investment limits. This wall of debt inflows was significant enough to substantially offset heavy foreign selling in equities that same month, and by some measures it pushed India's overall net FII flow for June into slightly positive territory despite the well-documented exodus from stocks. Falling oil prices reinforced the trend from a different angle: crude retreated from levels near $100 a barrel earlier in the month to the low $80s by its end, which eased both inflation worries and current-account concerns, giving yields room to grind lower even as geopolitical headlines continued to surface periodically.

Behind this surge in foreign appetite was a deliberate and fairly dramatic policy intervention by the Indian government. Through the Income-tax (Amendment) Ordinance, 2026, promulgated in early June with retrospective effect from April 1, 2026, authorities eliminated a set of tax burdens that had long made Indian sovereign debt less competitive relative to other emerging markets. The changes were substantial: the withholding tax on interest income, previously 20 percent, was reduced to zero; long-term capital gains tax, previously 12.5 percent, was eliminated entirely; and short-term capital gains tax, which could run as high as 30 percent, was likewise fully exempted. Importantly, these exemptions were narrowly targeted — they apply specifically to investments in government securities, including the expanded Fully Accessible Route tenors and Sovereign Green Bonds, but do not extend to corporate bonds, non-convertible debentures, or investments made by resident Indian citizens. Alongside the tax overhaul, the RBI also expanded the range of n tenors eligible under the Fully Accessible Route, adding another layer of accessibility for foreign capital. The rationale behind this reform was multi-pronged. Officials were aiming to shore up the rupee by making Indian bonds more attractive to global capital, thereby increasing demand for the currency and helping defend it against the depreciation pressures that had surfaced earlier in the year. There was also a longer-term ambition to deepen and diversify the bond market itself, reducing India's historical reliance on a relatively small pool of domestic institutional buyers and instead courting "sticky" long-term capital from sovereign wealth funds, pension funds, and insurance companies — investors far less prone to exiting abruptly during short-term turbulence. A further, and arguably more strategic, goal was clearing the path toward inclusion in major global bond indices, such as the Bloomberg Global Aggregate Bond Index; a tax-neutral investment environment is generally considered a prerequisite before passive global fund managers can allocate meaningfully to a sovereign debt market. Finally, policymakers were also eyeing the fiscal benefit: heavier foreign demand for government securities naturally exerts downward pressure on yields, which in turn lowers the government's own cost of borrowing. The market's response validated the strategy almost immediately. The record rush of foreign capital into Indian debt in June suggests the ordinance succeeded in removing much of the friction — the tangle of tax filings and treaty-based relief claims — that had previously discouraged international investors. In effect, Indian sovereign debt is now being priced and evaluated by global investors on largely the same terms as other major sovereign bond markets, marking one of the more consequential structural shifts in India's fixed-income landscape in recent years

The Indian bullion market witnessed a broad-based correction in June 2026, with both gold and silver extending their declines for a fourth consecutive month as global macroeconomic pressures outweighed intermittent safe-haven demand. Gold traded in a range-bound but softer trajectory throughout the month, while silver significantly underperformed, reflecting its greater sensitivity to both investment flows and industrial demand. Domestic gold prices eased from early June levels of around ₹148,000–151,500 per 10 grams to nearly ₹141,000–144,000 by the end of the month, while MCX gold futures remained relatively resilient, hovering near ₹153,500 per 10 grams. Overall, gold declined by approximately ₹7,000–10,000 per 10 grams during the month, with some market estimates suggesting a correction of nearly ₹15,000 from its peak. Silver experienced an even steeper fall, dropping from around ₹259,000–265,000 per kilogram in early June to nearly ₹240,000–245,000 by month-end, registering a decline of ₹15,000–25,000 per kilogram and marking one of its weakest monthly performances in over a decade. Several global and domestic factors contributed to the weakness in bullion prices. The strongest headwind came from a strengthening US dollar and elevated US Treasury yields as markets increasingly priced in a "higher-for-longer" interest rate environment from major central banks, particularly the US Federal Reserve. Rising real yields increased the opportunity cost of holding non-interest-bearing assets such as gold and silver, reducing investor appetite and triggering profit-booking after the metals had reached record highs earlier in 2026. Although geopolitical tensions in West Asia, particularly the Israel-Iran conflict, periodically revived safe-haven buying and lifted prices briefly, these rallies proved short-lived. Higher crude oil prices resulting from the conflict also reinforced inflation concerns, prompting expectations of tighter monetary policy that ultimately limited sustained gains in precious metals. Domestic market dynamics also remained challenging. The increase in gold import duty implemented in May had initially pushed local prices higher, but by June the market had largely adjusted to the new pricing regime. Elevated domestic prices, coupled with a depreciating rupee that raised import costs, discouraged fresh jewelery purchases during what is traditionally an off-season for demand between major wedding periods. Retail buying remained subdued, with many consumers preferring exchange-based purchases over fresh acquisitions. Dealers reported narrowing discounts compared with international landed prices, indicating that the market had reached a lower-demand equilibrium after the initial disruption caused by the duty hike. Investment demand also remained mixed, as gold exchange-traded funds recovered modestly after heavy outflows in May, but overall sentiment remained cautious. Silver's sharper correction reflected not only weaker investment demand but also growing concerns about the outlook for industrial consumption, particularly from sectors such as electronics, semiconductors and renewable energy. As expectations for global industrial growth moderated, silver's dual role as both a precious and industrial metal amplified its downside volatility. On commodity exchanges, traders adopted a cautious stance following the sharp correction witnessed in late May, with positioning remaining light amid continued uncertainty surrounding global interest rates, inflation and geopolitical developments. Overall, June 2026 marked a consolidation phase for the bullion market after the exceptional rally seen earlier in the year. While gold continued to outperform silver owing to its enduring safe-haven appeal, both metals remained under pressure from a stronger US dollar, elevated real interest rates, profit-taking by investors and subdued domestic demand. Looking ahead, bullion prices are likely to remain sensitive to developments in global monetary policy, geopolitical risks, currency movements and the revival of physical demand during the upcoming festive and wedding seasons.

In June 2026, the Indian rupee witnessed a relatively narrow but volatile trading pattern against the US dollar, with the currency gradually weakening as a stronger greenback and global risk aversion weighed on emerging market currencies. The rupee remained largely range-bound during the month but ended closer to the weaker side of its trading band as expectations of a more hawkish US Federal Reserve supported dollar demand.The monthly average exchange rate stood near ₹94.99 per US dollar, while the rupee traded around ₹94.33 on June 18 before slipping toward the ₹94.60–94.70 zone in the final weeks of the month. The primary factor driving rupee weakness was renewed strength in the US dollar, with the Dollar Index (DXY) hovering near 13-month highs around the 101 mark as markets priced in the possibility of a tighter US monetary policy stance. Higher-for-longer interest rate expectations increased the attractiveness of dollar assets, creating pressure on emerging market currencies, including the Indian rupee. Foreign institutional investor (FII) outflows from Indian equities and cautious domestic market sentiment further contributed to dollar demand, while importers’ hedging activity added to near-term selling pressure on the currency. However, the rupee’s decline remained controlled due to several supportive factors. Falling crude oil prices provided relief to India’s import bill, particularly after Brent crude eased toward the $75–76 per barrel range amid improving geopolitical sentiment and reduced concerns around supply disruptions. The moderation in oil prices helped partially offset the impact of dollar strength and prevented a sharper depreciation in the domestic currency. Market participants also pointed toward possible Reserve Bank of India (RBI) intervention as a stabilising factor. Dollar sales through state-owned banks and the central bank’s measured approach helped contain excessive volatility and maintained orderly market conditions. The RBI’s stance that discussions around rate hikes were premature, along with declining dollar-rupee forward premiums, suggested a cautious policy approach focused on managing liquidity and currency stability rather than aggressive tightening. Overall, June 2026 reflected a phase of gradual rupee depreciation rather than a disorderly decline. While global dollar strength, foreign outflows, and risk-off sentiment created headwinds, supportive crude trends, improving external conditions, and probable RBI intervention helped cushion the currency. The rupee’s performance highlighted the resilience of India’s external position despite a challenging global monetary environment.

Crude oil witnessed one of its sharpest reversals of 2026, transitioning from conflict-driven highs at the beginning of June to near pre-war levels by month-end. Brent crude, which started the month around US$95 per barrel amid heightened geopolitical tensions, fell more than 20% to the low-US$70s, while WTI slipped below US$70 for the first time since late February. The decline marked a dramatic unwinding of the risk premium that had built up following the Israel-US-Iran conflict, which began on February 28 and disrupted global energy markets. The conflict had pushed Brent above US$100 within days and to a peak of nearly US$126 by the end of April, as the effective closure of the Strait of Hormuz disrupted an estimated 14 million barrels of daily oil supply. Prices remained elevated through May, with fears of prolonged supply disruptions keeping markets on edge. Early June saw continued volatility as military exchanges between the US and Iran sustained concerns over regional stability. The turning point came in mid-June when reports emerged of a US-Iran memorandum of understanding aimed at reopening the Strait of Hormuz in exchange for easing sanctions and lifting restrictions on Iranian ports. Markets responded swiftly, with Brent losing nearly US$17 a barrel within days as investors anticipated a normalization of Middle East oil flows. By late June, tanker traffic through Hormuz had begun recovering, reinforcing expectations of improved supply. The correction was further supported by weaker global demand prospects, rising supply expectations from OPEC+ and the potential return of Iranian exports. Although sporadic attacks on vessels and delays in peace negotiations caused temporary price fluctuations, markets increasingly viewed these events as isolated rather than signs of renewed escalation. By the end of June, crude had largely shed its geopolitical premium, with prices once again being driven by underlying supply-demand fundamentals rather than conflict, setting a more balanced outlook for the second half of 2026.

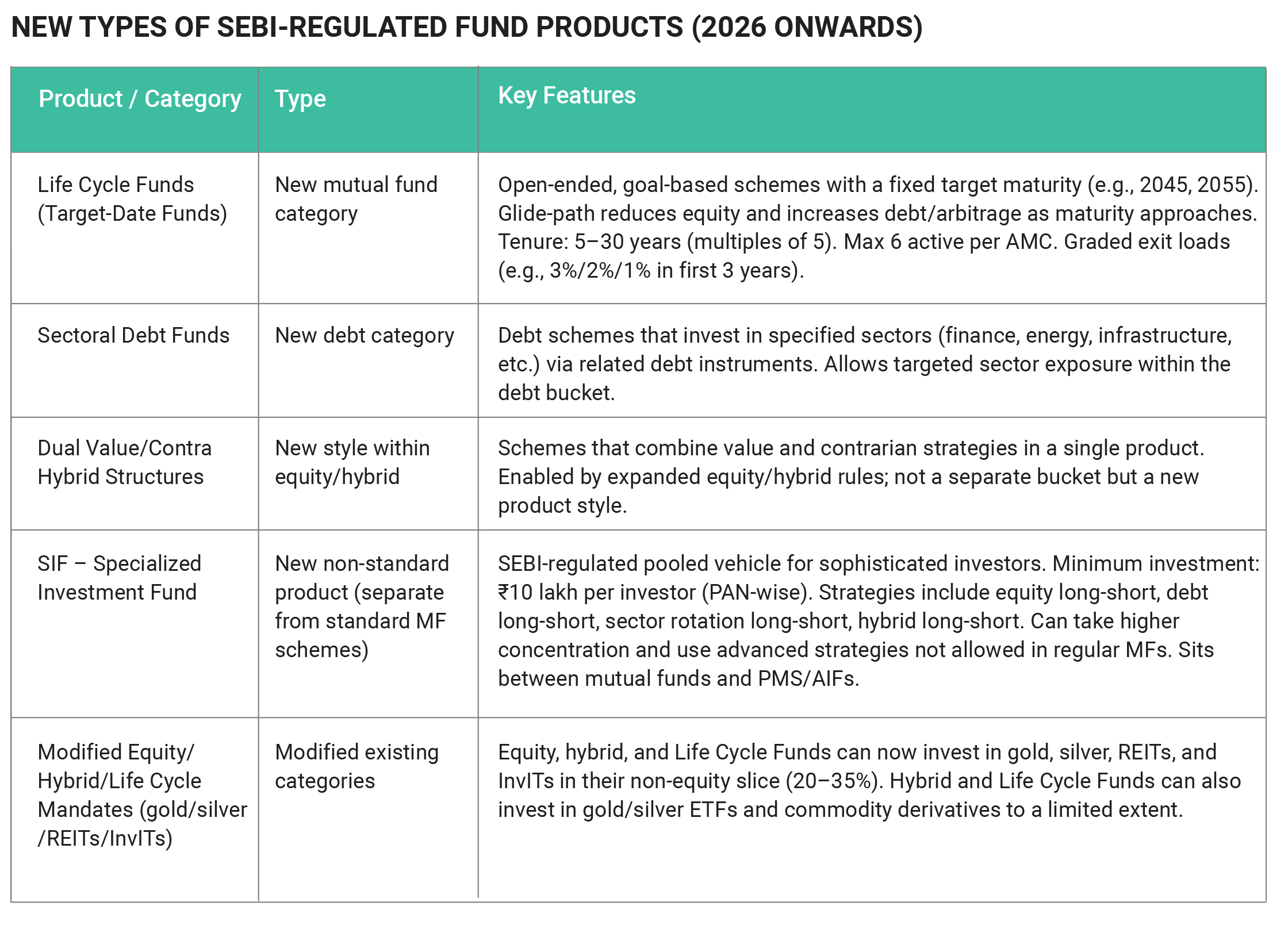

The Indian mutual fund industry witnessed a mixed month in June 2026, characterised by resilient retail participation despite subdued market returns and heightened global uncertainty. Equity fund inflows, which had already declined sharply in May amid volatility arising from the Israel-Iran conflict and elevated crude oil prices, remained softer in June as investors adopted a cautious stance. However, inflows continued to hover around their long-term average, reflecting sustained confidence in equities. Systematic Investment Plans (SIPs) remained the industry's biggest strength, with monthly contributions holding steady at nearly ₹31,000 crore. The resilience of SIPs highlighted investors' continued commitment to long-term wealth creation despite short-term market fluctuations. Nevertheless, the industry faced a significant challenge as equity fund returns remained largely muted over the past year, with many active funds still below their previous highs and trailing debt funds on a one-year rolling basis. The month also saw continued product innovation. Asset management companies expanded their passive and goal-based offerings through new index funds and India's first target-date (life-cycle) funds following SEBI's new regulatory framework. Meanwhile, SEBI's proposal to introduce performance-linked fund management fees sparked industry-wide discussions on better aligning fund manager incentives with investor outcomes. Alongside regulatory updates, several AMCs announced fund mergers, management changes and operational enhancements, underscoring the industry's focus on innovation, efficiency and long-term investor engagement.