Topic 1: EQUITY: STEADY CURRENTS

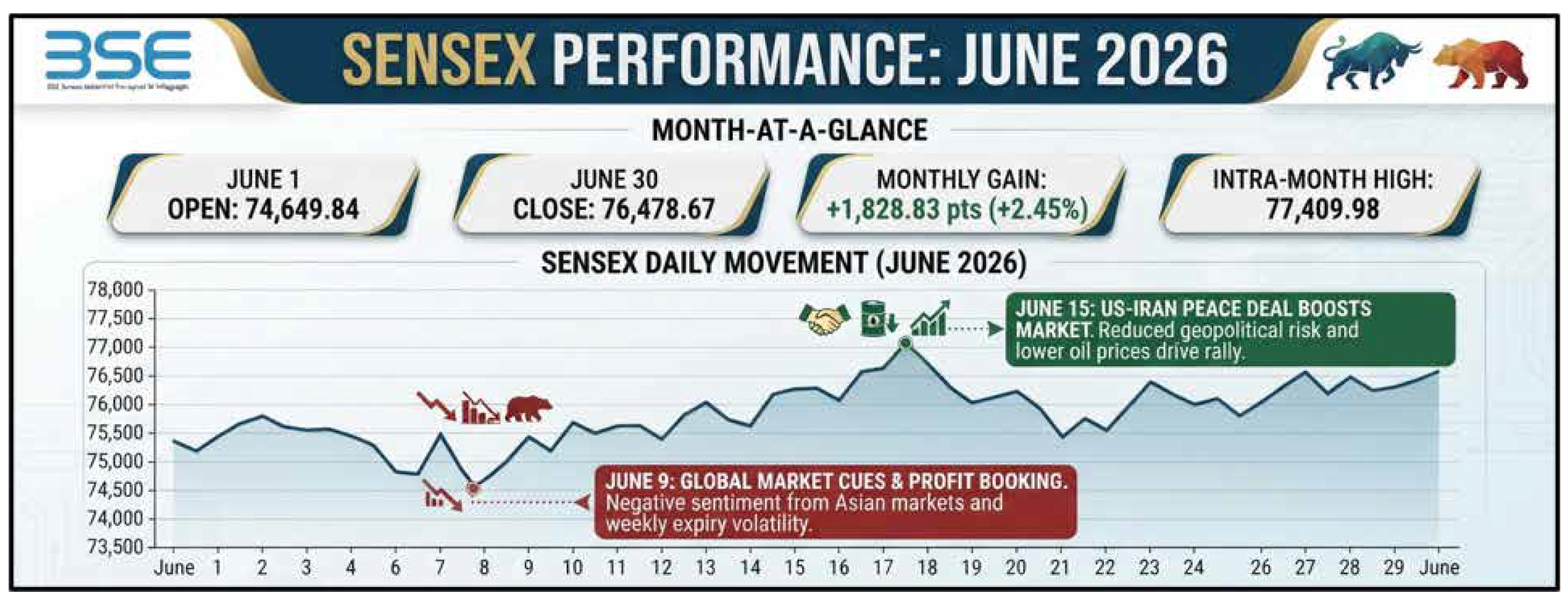

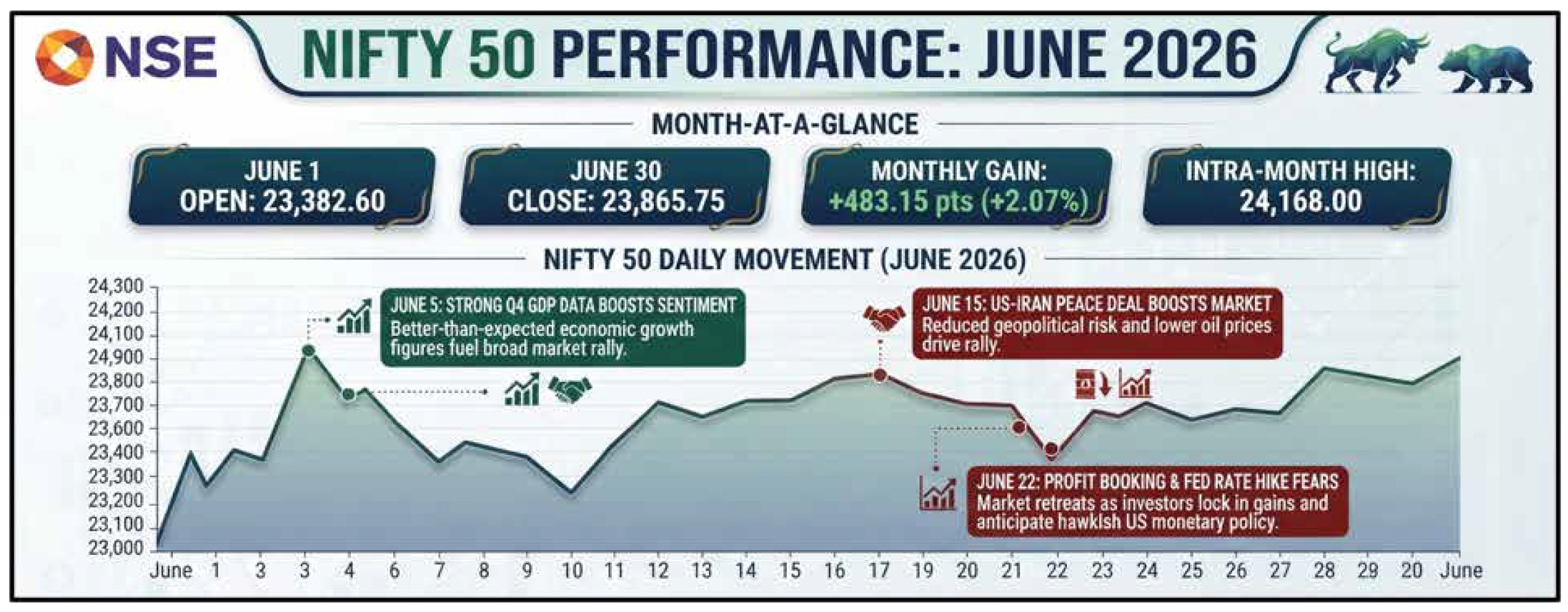

India's equity markets ended June 2026 on a positive note despite experiencing one of the most volatile months of the year. The BSE Sensex closed at 76,478.67, gaining 1,702.93 points (2.28%), while the NSE Nifty 50 finished at 23,865.75, up 483.15 points (2.07%). Although the benchmark indices posted modest gains, the broader market displayed greater resilience, with mid- and small-cap stocks outperforming large caps as domestic investors increasingly favored higher-beta, India-focused companies. Throughout the month, markets were influenced by a complex mix of domestic monetary policy, geopolitical developments in West Asia, global risk sentiment, and contrasting institutional investment flows. The month began with the Reserve Bank of India keeping the repo rate unchanged at 5.25%, but the accompanying downgrade in FY27 GDP growth projections and upward revision to inflation expectations reinforced a "higher-for-longer" interest rate outlook, tempering investor optimism. Geopolitical tensions soon became the dominant market driver. Escalating conflict between Israel and Iran, including military strikes and fears of disruption around the Strait of Hormuz, pushed crude oil prices close to US$100 per barrel during the first week of June. The resulting spike in oil prices triggered a sharp sell-off in Indian equities on 5 June, with the Sensex and Nifty falling around 1% to multi-month lows. A temporary easing of hostilities over the following days allowed

crude prices to retreat, enabling Indian markets to recover, led by banking and broader market stocks. Fresh concerns emerged around 10 June, when the United States expanded military operations against Iranian targets, reviving fears of a wider regional conflict. However, sentiment improved during the second half of the month as reports of a potential US-Iran ceasefire and diplomatic negotiations reduced concerns over prolonged disruptions to global energy supplies. Markets responded positively to these developments, although intermittent reports of ceasefire violations and tensions around the Strait of Hormuz continued to create bouts of volatility. Another major setback occurred on 23 June, when a global risk-off wave coinciding with weekly options expiry and an unexpected double-digit decline in South Korea's KOSPI index triggered widespread selling across Asian markets, including India. Defensive sectors such as pharmaceuticals outperformed during this period as investors sought safer assets. Renewed US military strikes on Iranian missile and radar installations later in the month generated only a muted market reaction, indicating that investors had begun pricing in recurring geopolitical flare-ups rather than anticipating a full-scale regional conflict. Nevertheless, profit booking in the final trading sessions, particularly in technology stocks, resulted in modest declines on the last day of June. Sectoral performance reflected significant rotation within the market. Banking was the strongest performer, with the BSE Bankex rising 6.38%, supported by expectations of stable interest rates, improving credit growth, and stronger earnings visibility. Realty stocks also gained 5.86%, benefiting from supportive financing conditions and resilient housing demand. In contrast, metals emerged as the weakest sector, declining 8.15% amid global growth concerns and volatile commodity prices. Technology stocks also underperformed, with the BSE Teck Index falling 5.84%, as investors remained concerned about slowing global IT spending, elevated valuations, and the long-term impact of artificial intelligence on traditional outsourcing business models. Auto and PSU banking stocks witnessed mixed performance towards the month-end as leadership continued rotating across sectors. One of the defining characteristics of June was the stark divergence between foreign and domestic institutional investors. Foreign Institutional Investors (FIIs) remained persistent sellers, recording their twelfth consecutive month of net outflows with approximately ₹49,028 crore withdrawn from Indian equities due to concerns over US interest rates, currency movements, and global asset allocation. In contrast, Domestic Institutional Investors (DIIs) invested around ₹85,800 crore, supported by strong mutual fund SIP inflows, insurance companies, pension funds, and other long-term domestic investors. This consistent domestic buying repeatedly cushioned the market against foreign selling and external shocks, demonstrating the growing maturity and resilience of India's capital markets. Even on the final trading day of the month, DIIs significantly outpaced FII selling, reinforcing domestic liquidity as the primary support for equities. Overall, June 2026 highlighted the increasing ability of Indian markets to absorb external geopolitical risks, tighter monetary conditions, and global volatility while still delivering positive monthly returns. The combination of strong domestic participation, sectoral rotation, resilient banking stocks, and sustained retail inflows enabled Indian equities to withstand repeated bouts of uncertainty, reinforcing confidence in the long-term structural strength of the market despite a challenging global environment.