Topic 2: DEBT: CAPITAL BRIDGE

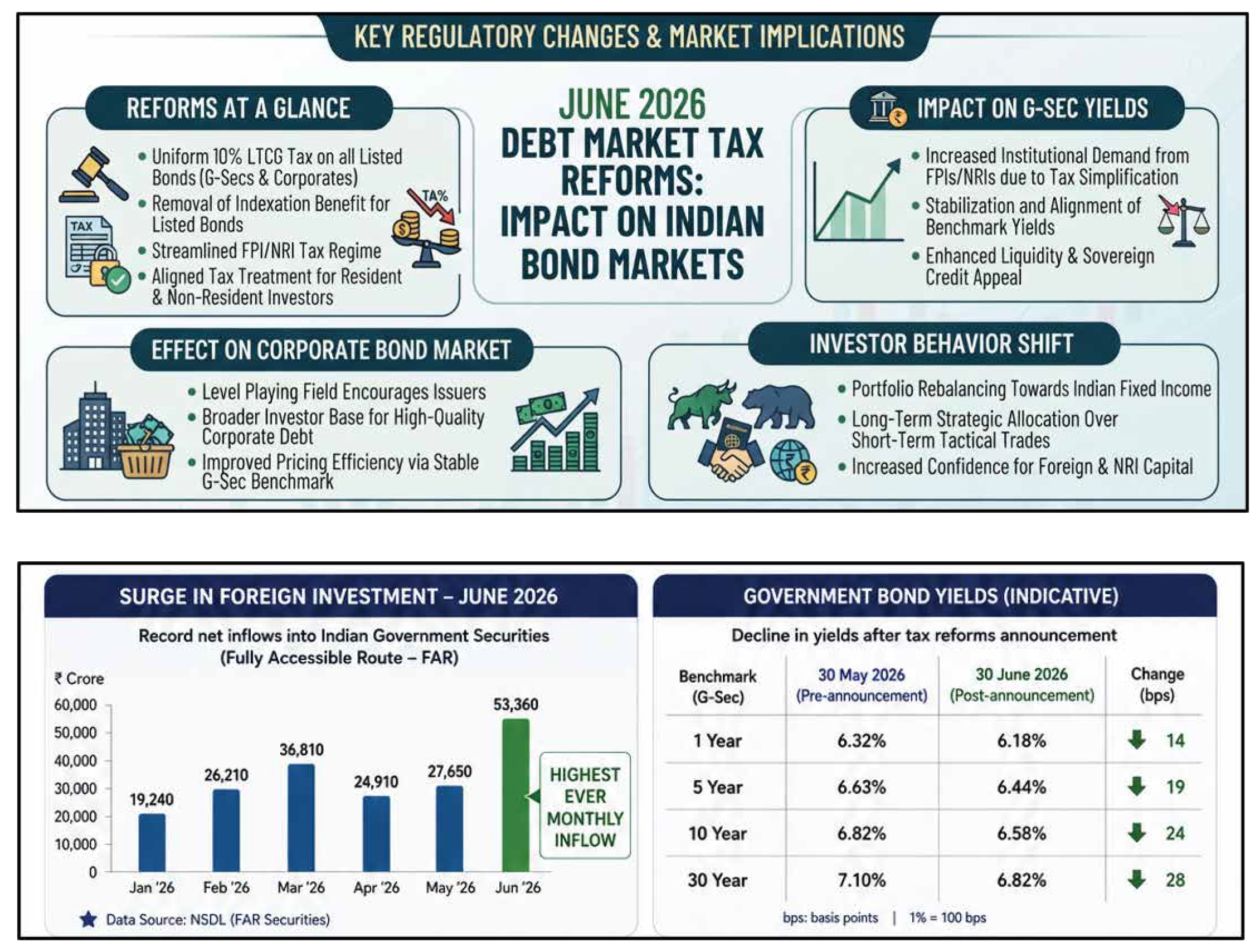

India's debt markets turned in a strikingly strong performance in June 2026, standing in sharp contrast to the choppier mood in equities that month. The headline move was in government securities, where the 10-year benchmark yield slid from around 7.02 percent at the end of May to roughly 6.75-6.77 percent by late June, a meaningful drop driven by a wave of record foreign inflows and a retreat in crude oil prices that improved both the inflation outlook and the rupee's standing. This wasn't confined to the long end of the curve either — the money market, which had been under real stress in May, normalized considerably. With the Reserve Bank of India holding its repo rate steady at 5.25 percent and liquidity conditions easing, certificate of deposit yields fell sharply, dropping around 60 basis points to settle near 7.0 percent. Perhaps more tellingly, the front end of the yield curve, which had been unusually inverted — with very short-tenor instruments yielding more than 1-3 year paper — began to unwind, restoring a more conventional upward-sloping term structure. Corporate bonds joined the rally too, buoyed by improved liquidity and firm demand at the higher-rated end of the market, with primary issuance picking up and spreads holding relatively tight at around 500 basis points for the broader market, even though episodic risk-off days tied to tensions in West Asia kept investors somewhat selective about where they deployed capital. The single biggest force behind this rally was the behavior of foreign investors, who poured money into Indian debt at a scale rarely seen before. Foreign portfolio investors funneled a record amount into the market during June — figures vary slightly depending on the source, with some accounts citing approximately ₹53,300 crore with the bulk of that capital flowing into government bonds and treasury bills through the Fully Accessible Route and other general investment limits. This wall of debt inflows was significant enough to substantially offset heavy foreign selling in equities that same month, and by some measures it pushed India's overall net FII flow for June into slightly positive territory despite the well-documented exodus from stocks. Falling oil prices reinforced the trend from a different angle: crude retreated from levels near $100 a barrel earlier in the month to the low $80s by its end, which eased both inflation worries and current-account concerns, giving yields room to grind lower even as geopolitical headlines continued to surface periodically. Behind this surge in foreign appetite was a deliberate and fairly dramatic policy intervention by the Indian government. Through the Income-tax (Amendment) Ordinance, 2026, promulgated in early June with retrospective effect from April 1, 2026, authorities eliminated a set of tax burdens that had long made Indian sovereign debt less competitive relative to other emerging markets. The changes were substantial: the withholding tax on interest income, previously 20 percent, was reduced to zero; long-term capital gains tax, previously 12.5 percent, was eliminated entirely; and short-term capital gains tax, which could run as high as 30 percent, was likewise fully exempted. Importantly, these exemptions were narrowly targeted — they apply specifically to investments in government securities, including the expanded Fully Accessible Route tenors and Sovereign Green Bonds, but do not extend to corporate bonds, non-convertible debentures, or investments made by resident Indian citizens. Alongside the tax overhaul, the RBI also expanded the range of tenors eligible under the Fully Accessible Route, adding another layer of accessibility for foreign capital. The single biggest force behind this rally was the behavior of foreign investors, who poured money into Indian debt at a scale rarely seen before. Foreign portfolio investors funneled a record amount into the market during June — figures vary slightly depending on the source, with some accounts citing approximately ₹53,300 crore with the bulk of that capital flowing into government bonds and treasury bills through the Fully Accessible Route and other general investment limits. This wall of debt inflows was significant enough to substantially offset heavy foreign selling in equities that same month, and by some measures it pushed India's overall net FII flow for June into slightly positive territory despite the well-documented exodus from stocks. Falling oil prices reinforced the trend from a different angle: crude retreated from levels near $100 a barrel earlier in the month to the low $80s by its end, which eased both inflation worries and current-account concerns, giving yields room to grind lower even as geopolitical headlines continued to surface periodically.

Behind this surge in foreign appetite was a deliberate and fairly dramatic policy intervention by the Indian government. Through the Income-tax (Amendment) Ordinance, 2026, promulgated in early June with retrospective effect from April 1, 2026, authorities eliminated a set of tax burdens that had long made Indian sovereign debt less competitive relative to other emerging markets. The changes were substantial: the withholding tax on interest income, previously 20 percent, was reduced to zero; long-term capital gains tax, previously 12.5 percent, was eliminated entirely; and short-term capital gains tax, which could run as high as 30 percent, was likewise fully exempted. Importantly, these exemptions were narrowly targeted — they apply specifically to investments in government securities, including the expanded Fully Accessible Route tenors and Sovereign Green Bonds, but do not extend to corporate bonds, non-convertible debentures, or investments made by resident Indian citizens. Alongside the tax overhaul, the RBI also expanded the range of n tenors eligible under the Fully Accessible Route, adding another layer of accessibility for foreign capital. The rationale behind this reform was multi-pronged. Officials were aiming to shore up the rupee by making Indian bonds more attractive to global capital, thereby increasing demand for the currency and helping defend it against the depreciation pressures that had surfaced earlier in the year. There was also a longer-term ambition to deepen and diversify the bond market itself, reducing India's historical reliance on a relatively small pool of domestic institutional buyers and instead courting "sticky" long-term capital from sovereign wealth funds, pension funds, and insurance companies — investors far less prone to exiting abruptly during short-term turbulence. A further, and arguably more strategic, goal was clearing the path toward inclusion in major global bond indices, such as the Bloomberg Global Aggregate Bond Index; a tax-neutral investment environment is generally considered a prerequisite before passive global fund managers can allocate meaningfully to a sovereign debt market. Finally, policymakers were also eyeing the fiscal benefit: heavier foreign demand for government securities naturally exerts downward pressure on yields, which in turn lowers the government's own cost of borrowing. The market's response validated the strategy almost immediately. The record rush of foreign capital into Indian debt in June suggests the ordinance succeeded in removing much of the friction — the tangle of tax filings and treaty-based relief claims — that had previously discouraged international investors. In effect, Indian sovereign debt is now being priced and evaluated by global investors on largely the same terms as other major sovereign bond markets, marking one of the more consequential structural shifts in India's fixed-income landscape in recent years