Topic 2: DEBT: YIELD SHOCK

In April 2026, India’s debt markets faced a broad-based

selloff as yields repriced sharply upward in response to

geopolitical tensions in West Asia, rising crude oil prices,

and mounting inflation concerns. This environment

proved particularly challenging for interest

rate–sensitive instruments, especially government

securities (G-secs) and long-duration debt funds. As

yields climbed across the curve, bond prices declined,

leading to negative returns in several fixed-income

categories. However, the impact was not

uniform—shorter-duration instruments and

credit-oriented products displayed relative resilience,

supported by lower duration risk and stable credit

spreads.

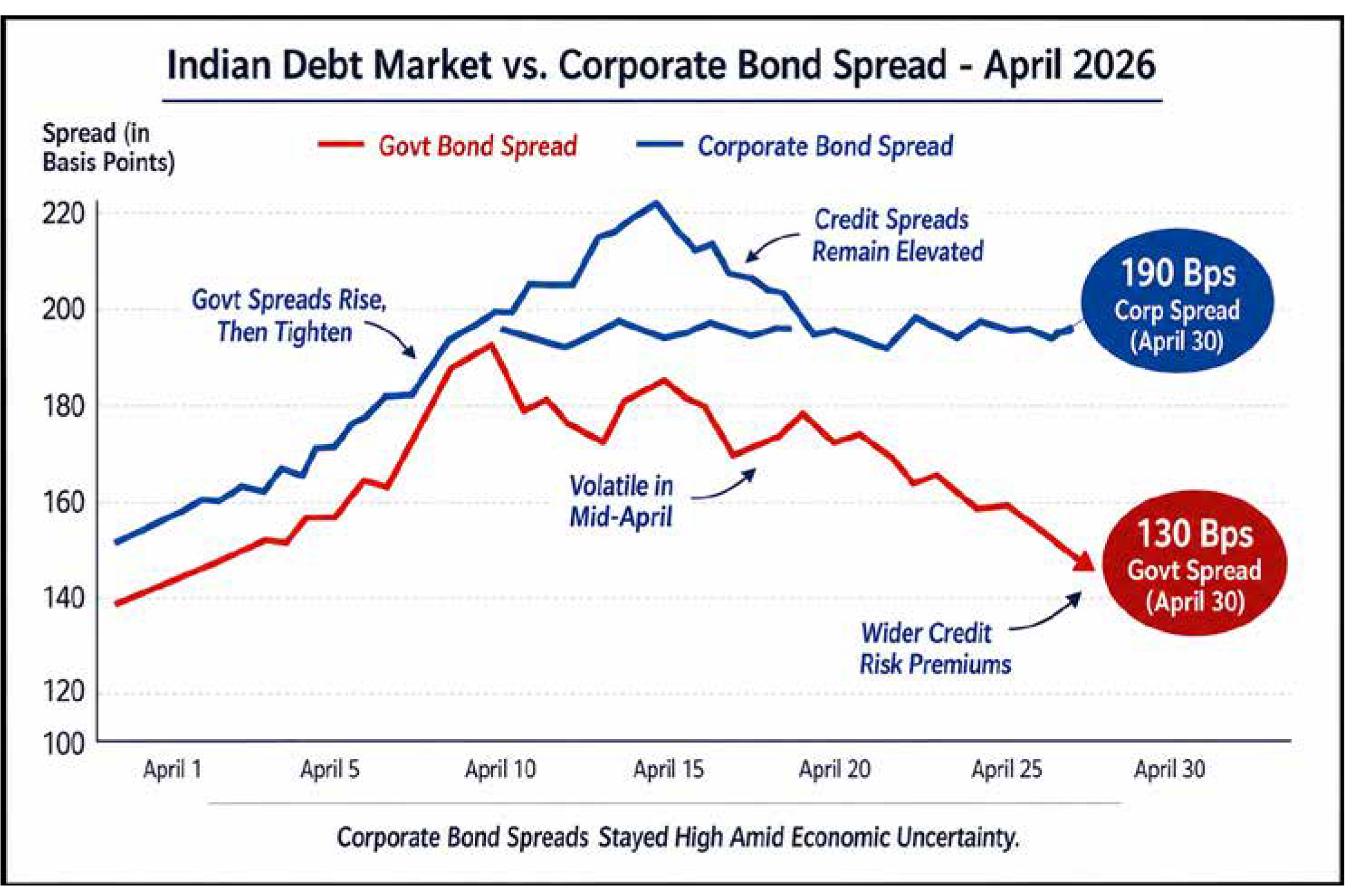

Government securities bore the brunt of the adjustment.

The 10-year benchmark yield rose significantly, moving

from roughly 6.6–6.7% in early March to around

6.9–7.0% by late April, even touching a two-week high of

approximately 6.98% in mid-April. This upward

movement reflected a reassessment of inflation risks

and expectations of tighter monetary conditions.

Notably, the repricing was more pronounced at the short to mid-end of the yield curve. Yields on 2-year and 3-year

G-secs climbed steadily as markets began pricing in

near-term inflation pressures and the likelihood of

liquidity tightening by the Reserve Bank of India (RBI).

Similarly, 5-year bonds experienced upward pressure as

traders positioned for a less accommodative liquidity

environment. At the long end, 20- to 30-year bonds

underperformed further, as investors demanded higher

term premiums to compensate for fiscal uncertainties

and persistent inflation risks.

Corporate bond markets also reflected the broader

tightening in financial conditions, though with variations

across credit quality and sectors. Investment-grade

corporate bonds experienced moderate price pressure,

but in some cases, spreads tightened slightly, especially

in sectors linked to India’s capital expenditure cycle. This

resulted in largely flat to mildly negative returns for

top-rated instruments. In contrast, lower-rated or

high-yield bonds faced greater stress. Investors grew

increasingly cautious amid rising borrowing costs and

heightened volatility, leading to wider spreads and

weaker secondary market prices for these issuers.

Several interrelated factors drove these developments.

Foremost among them was the escalation of

geopolitical tensions in West Asia, which pushed Brent

crude oil prices sharply higher, in some instances

approaching or exceeding $100 per barrel. For an

oil-importing country like India, this translated into fears

of imported inflation, with potential knock-on effects on

both consumer and wholesale price indices. As inflation

expectations rose, markets began to anticipate a more

hawkish stance from the RBI, including the possibility of

prolonged higher policy rates. This led to a front-loading

of rate expectations, particularly impacting shorter-tenor

bonds.

At the same time, global bond markets experienced a

surge in volatility, reflected in rising rate volatility

indicators similar to the MOVE index. Yield curves

flattened globally, but at higher absolute levels, signalling

that investors were demanding greater compensation

for uncertainty. Indian bond markets followed suit, with

the rise in the 10-year yield reflecting not just inflation

expectations but also an increase in term premiums.

Liquidity and fiscal concerns further amplified the

upward pressure on yields. Expectations of tighter

domestic liquidity—driven by a higher import bill,

potential capital outflows during risk-off conditions, and

pressure on money market rates—made short-term

instruments more sensitive to rate changes. Meanwhile,

concerns about fiscal slippage, including higher

government spending on energy subsidies and possible

war-related expenditures, pushed long-term yields higher

as investors reassessed India’s fiscal trajectory.

Despite these pressures, the RBI played a stabilizing role

in the market. Through targeted open market operations

and secondary market purchases of government bonds,

the central bank helped anchor the 10-year yield,

preventing excessive volatility. However, this support

was concentrated around the benchmark segment,

leaving shorter- and longer-tenor bonds more exposed to

market-driven repricing.

Investor behaviour also influenced market outcomes.

Retail and institutional investors increasingly shifted

allocations toward shorter-duration and credit-focused

funds, seeking to mitigate interest rate risk. These flows

helped stabilize segments of the market and prevented a

disorderly selloff. However, investors with exposure to

long-duration gilt funds faced significant mark-to-market

losses, as rising yields eroded bond prices despite steady

coupon income.

In the corporate bond segment, yield movements closely

tracked changes in government bond yields but were

further influenced by credit risk considerations.

Top-rated AAA and A1 issuers saw yields rise by around

20–30 basis points, while BBB-rated and lower-quality

issuers experienced more substantial increases of

40–60 basis points or more. Sectoral differences were

also evident. Industries heavily dependent on crude oil or

global trade—such as aviation, shipping, refining, and

certain manufacturing segments—saw sharper yield

increases due to concerns about margin compression

and earnings volatility. Conversely , defensive sectors

like large public sector enterprises, regulated utilities,

and select financial institutions experienced more

moderate yield movements, supported by stable cash

flows and, in some cases, implicit government backing.

In essence, April 2026 underscored the vulnerability of

debt markets to external shocks and the critical

importance of duration management. While rising yields

created near-term pain through capital losses, they also

reset the yield environment to more attractive levels for

future investors, particularly in shorter-duration and

high-quality segments.